The Billion-User Crash: Why Mobile Banking App Testing Is Your Only Safety Net

Mobile is no longer an alternative channel; for most customers, it is the bank. By the end of 2025, 2.17 billion people globally are estimated to manage their finances exclusively through screens that fit in their pockets. Mobile banking app testing is the rigorous process of verifying the functionality, security, and performance of financial applications to ensure they withstand regulatory scrutiny and intense user demand.

In the fintech domain, a glitch isn’t just a technical annoyance; it is a breach of trust. With 72% of U.S. adults relying on these tools, the tolerance for error has evaporated. A single bug can cause financial losses, trigger regulatory fines, and destroy customer loyalty in seconds. The data supports this volatility: 94% of users uninstall a new app within 30 days if they encounter bugs or sluggish performance.

This high-stakes environment demands more than basic functionality checks. It requires a strategic approach to fintech app testing that prioritizes digital trust. This comprehensive guide provides the framework to overcome complex industry challenges, leveraging AI-driven automation and real-device testing to accelerate quality and secure the user experience.

The 4 Silent Killers of Banking App Reliability

Mobile banking app testing is uniquely brutal. Unlike an e-commerce store or a social media feed, financial applications do not have the luxury of “fail fast and fix later.” The combination of high financial stakes, complex security vulnerabilities, and the demanding real-time nature of financial services creates a hostile environment for quality assurance.

Here is why standard testing strategies often crumble in the fintech sector.

1. The Trap of Intricate Business Workflows

Banking workflows are rarely linear. A user does not simply “add to cart” and “checkout.” They apply for loans, transfer funds, and manage investments in workflows that span over 15 integrated systems and require multiple approvals. A loan application might start on a mobile device, pause for manual underwriting, and conclude with a digital signature days later.

Testing these paths requires rigorous end-to-end validation. You must verify not just the “happy path” but every negative test case, such as a connection drop during a fund transfer or a session timeout during a mortgage application. If your Banking mobile app QA strategy isolates these steps, you miss the integration bugs that actually cause crashes.

2. The “Black Box” of Third-Party Integrations

Modern banking apps are essentially polished interfaces sitting on top of a web of third-party dependencies. Your app relies on external APIs for KYC verification, credit bureau checks, and payment gateways like Zelle or UPI.

The problem? You cannot control these external systems. If a third-party credit check API fails, your user sees a broken app and blames your bank. Fintech app testing must include API virtualization and mocking to simulate these failures. This isolates your core functionality, ensuring that if a partner goes down, your app handles the error gracefully rather than crashing.

3. Economic Panic and the Load Spike

Financial apps face unpredictable traffic patterns that defy standard capacity planning. We call this “Economic Panic Load.” Traffic does not just spike on Black Friday; it spikes when paydays align with holidays, during market crashes, or following major economic announcements.

To survive, performance testing for mobile apps must go beyond average load expectations. Banks typically need to simulate up to 50,000 transactions per minute to validate stability. More importantly, teams must test for Recovery Time Objectives (RTO)—measuring exactly how many seconds it takes for the system to recover after a catastrophic failure during these peaks.

4. The Compliance and Fragmentation Vice

Testing teams operate in a vice grip between rigid regulations and infinite hardware variables.

- The Regulatory Burden: You are not just testing for bugs; you are testing for the law. Mandates like PCI DSS, GDPR, and the EU’s Digital Operational Resilience Act (DORA) are non-negotiable. A single lapse in security testing for mobile financial apps—such as exposed data in a log file—can trigger massive fines.

- Device Fragmentation: The hardware reality is chaotic. There are over 24,000 distinct Android devices globally. Supporting every device is impossible, yet Real-device mobile banking testing is essential because emulators cannot accurately replicate biometric sensors or battery drain on older models. The most effective teams focus on a matrix of 20–40 high-market-share devices to maintain crash-free rates above 99%.

The Core Disciplines of Mobile Banking App Testing

A comprehensive test strategy in banking does not just look for bugs; it prioritizes financial risk. While a UI glitch in a gaming app is annoying, a calculation error in a loan repayment schedule is a lawsuit. Therefore, mobile banking app testing must fuse multiple disciplines, placing security and data integrity above feature velocity.

1. Security and Compliance: The DevSecOps Approach

Security cannot be a final hurdle cleared days before release. It must be embedded into the development lifecycle—a practice known as Shift-Left Security. Security testing for mobile financial apps is the single most critical area, focusing on preventing unauthorized access and financial fraud.

Modern strategies move beyond basic checks to rigorous automated standards:

- Vulnerability Assessment: Teams must automate scanning for common threats like SQL injection and Cross-Site Scripting (XSS). This also includes detecting “Screen Overlay Attacks,” where malware hijacks user input by placing a fake layer over legitimate banking apps.

- Authentication & Biometrics: You must rigorously validate Multi-Factor Authentication (MFA) and biometric logins (Face ID/fingerprint). This includes ensuring secure session termination so that a stolen phone doesn’t grant open access to a bank account.

- Compliance Verification: Adherence to the OWASP MASVS (Mobile Application Security Verification Standard) is now the industry benchmark. Furthermore, institutions operating in Europe must prepare for the Digital Operational Resilience Act (DORA), which mandates strict evidence of digital resilience.

2. Test Data Management (TDM) and Privacy

One of the biggest bottlenecks in banking mobile app QA is data. Testing requires realistic transaction histories to validate complex workflows, but using production data violates privacy laws like GDPR and CCPA.

You cannot simply copy a production database for testing. The solution lies in synthetic data generation and PII masking. Teams create “fake” user profiles with valid credit card formats and logical transaction histories. This ensures that even if a test log is exposed, no real customer data is compromised. Effective TDM ensures you can test edge cases—like a user with negative balance attempting a transfer—without risking customer privacy.

3. Performance and Load Testing (The Panic Check)

Your app works fine with 100 users, but what happens on payday? Performance testing for mobile apps ensures the application remains responsive during massive, concurrent usage.

- Load Testing: You must simulate large numbers of concurrent users accessing the app to identify bottlenecks. Banks often simulate up to 50,000 transactions per minute to stress-test backend systems.

- Transaction Speed: Users expect real-time results. Testing must enforce strict Service Level Objectives (SLOs) for critical features like fund transfers. A delay of just 1-2 seconds can cause 18% of users to abandon the app.

- Network Shaping: Real users do not always have perfect 5G. You must test for graceful degradation across spotty Wi-Fi, low 4G, and roaming connections to ensure the app handles timeouts without crashing.

4. UX and Accessibility: The Legal & Trust Necessity

Usability is a survival metric. With 46% of customers willing to switch banks for a better digital experience, friction is a business risk. Mobile banking UX testing goes beyond aesthetics; it validates that a non-technical user can complete a transfer without anxiety.

Crucially, accessibility is a legal mandate. Courts increasingly view digital banking as a public accommodation. You must validate compliance with WCAG 2.1 standards, ensuring support for screen readers (VoiceOver/TalkBack), sufficient color contrast, and focus management. This ensures inclusivity and protects the institution from discrimination lawsuits.

5. Interruption Testing: The Reality Check

Mobile phones are chaotic environments. What happens to a wire transfer if a phone call comes in exactly when the user hits “Submit”? Interruption testing simulates these real-world intrusions—incoming calls, low battery alerts, or network loss. The app must handle these gracefully, ensuring the transaction is either completed or safely cancelled without “zombie” data remaining in the system.

Automation and Real Devices—The Modern Solution

Manual regression testing in fintech is a losing battle. With weekly release cycles and app stores demanding perfection, human speed cannot keep up with the technical debt. Mobile financial app automation is no longer a luxury; it is the definitive answer to the massive regression and speed demands of the fintech space.

Organizations that successfully implement automation report a 60%+ reduction in test execution effort and 50% faster regression testing cycles. However, speed is worthless without accuracy. The modern solution requires a dual strategy: rigorous automation frameworks and a refusal to compromise on hardware reality.

1. The Automation Imperative: Frameworks and AI

The foundation of a robust strategy lies in choosing the right tools. While mobile banking native app automation often relies on platform-specific tools like XCUITest (iOS) and Espresso (Android) for their speed and deep system access, cross-platform solutions like Appium remain the industry standard for their flexibility.

But tools alone do not solve the maintenance nightmare. A common failure point in automation is a fragile locator strategy (XPath, CSS selectors, accessibility locators). Banking apps frequently update their UI for compliance or marketing, breaking rigid scripts that rely on static XPaths.

This is where AI transforms the workflow. AI-driven automation now offers “Self-Healing Scripts,” where intelligent agents automatically adjust locators when UI elements shift, drastically reducing script maintenance. Instead of a test failing because a “Submit” button moved two pixels, the AI recognizes the button by its attributes and proceeds, keeping the pipeline green.

2. Real Devices vs. Emulators: Why Accuracy Matters

For real-device mobile banking testing, emulators are useful for early logic checks, but they are dangerous for final validation. An emulator is a software mimic; it cannot replicate the thermal throttling of a CPU, the interference of a subway tunnel, or the specific behavior of a Samsung OneUI skin versus a Google Pixel interface.

For banking apps specifically, reliance on emulators leaves massive blind spots. You cannot test FaceID integration or NFC “tap-to-pay” functionality on a simulated screen. The following table highlights why real hardware is non-negotiable for financial apps:

| Aspect | Emulator/Simulator | Real Device Testing | Criticality for Banking Apps |

| Biometrics | Limited support | Full access (Face ID, Fingerprint, Iris) | Essential for secure login and payment authorizations. |

| Beta OS Testing | None/Delayed | Install Beta iOS/Android versions | Critical to prevent “Day 1” crashes when Apple or Google release new OS updates. |

| Network Conditions | Simulated (perfect logic) | Actual Cellular/Wi-Fi/Roaming | High Importance to test transaction resilience during handovers (e.g., leaving Wi-Fi). |

| Manufacturer UI | Generic Android | Specific Skins (OneUI, MIUI, OxygenOS) | High Importance to catch vendor-specific bugs that hide behind custom OS overlays. |

By combining resilient automation frameworks with a robust real-device lab, banking QA teams move from “hoping it works” to knowing it will perform.

The Infrastructure of Trust—Accelerating Quality with Qyrus

To meet the speed and security demands of mobile banking app testing, a modern strategy requires more than just scripts; it demands a robust infrastructure capable of running complex scenarios on real-world hardware. Qyrus directly addresses this with its specialized Mobile Testing solution and dedicated Device Farm.

Solving “Intricate Workflows” with Biometric Bypass

A major bottleneck in mobile banking native app automation is the security gate itself. Automating a login flow often hits a wall when the app demands FaceID or a fingerprint. Most tools cannot bypass this, forcing testers to manually intervene or skip secure login tests entirely.

Qyrus solves this with its Instrumentation Feature, which allows testers to bypass biometric authentication prompts on real devices. This capability is critical for Fintech app testing, as it enables end-to-end automation of secure workflows—like transferring funds or viewing statements—without manual hand-holding. This feature works on instrumentable debug builds for Android, directly addressing the “Intricate Business Workflows” challenge identified earlier.

Learn more about mobile app testing with Qyrus

Mastering Fragmentation and Digital Inclusion

You cannot validate a banking app’s stability on a single iPhone. The Qyrus Device Farm provides an all-in-one platform that eliminates the need for maintaining costly physical device inventories.

- Real-Device Confidence: The platform provides live access to a diverse set of real smartphones and tablets, backed by a 99.9% availability promise. This supports Real-device mobile banking testing across a wide range of operating systems, including day-one support for Android 16 and iOS 26 beta.

- Digital Inclusion via Network Shaping: Banking must be accessible to everyone, not just users with high-speed fiber. Qyrus allows testers to simulate adverse network conditions—such as 2G speeds, high latency, or packet loss. This ensures the app handles the “Economic Panic Load” without crashing, serving rural users as effectively as urban ones.

Advanced Financial Testing Capabilities

Qyrus integrates specialized features that cater specifically to the high-stakes nature of banking mobile app QA:

- Interrupt Testing: Users rarely bank in a vacuum. Qyrus enables you to simulate phone calls and text messages during active sessions to check if the application crashes or maintains its state.

- AI-Powered Exploration (Rover): To expand coverage beyond written scripts, Rover AI utilizes deep reinforcement learning for autonomous exploratory testing. It generates unlimited test cases to find edge cases a human might miss.

- Resilient Automation (Healer AI): Banking UIs change frequently. The Healer AI automatically adjusts your locator strategy (XPath, CSS selectors, accessibility locators) when UI elements shift. If a “Transfer” button ID changes, the AI finds the new locator, ensuring mobile financial app automation remains unbroken.

The Strategic Layer: Unifying Quality

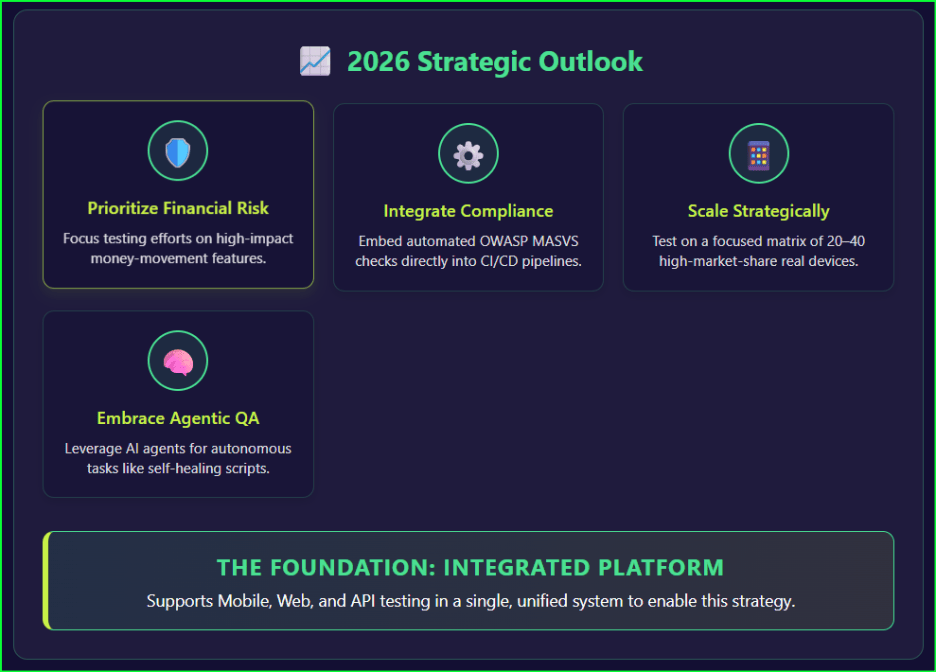

Siloed testing creates blind spots. Qyrus operates as a unified component that supports cross-platform mobile/web UI testing and API testing within a single interface.

This integration allows for security testing for mobile financial apps and performance testing for mobile apps to occur alongside functional checks. The platform feeds seamless results into overarching systems, supporting collaboration through integrations with Jira, Azure DevOps, and Jenkins. By consolidating Web, API, and Mobile testing, Qyrus ensures that the backend API failure discussed in Chapter 1 is caught just as quickly as a frontend UI glitch.

Strategic Takeaways and Future Focus (2026 Outlook)

The future of mobile banking app testing is not just about finding bugs faster; it is about predicting them before code is even committed. As we move through 2025, the industry is shifting away from reactive quality assurance toward proactive, AI-driven risk management.

To stay competitive and secure, financial institutions must pivot their strategies around these four pillars.

1. Prioritize Financial Risk Over Feature Parity

You cannot test everything with equal intensity. A font misalignment on a “About Us” page is a cosmetic issue; a failure in the “Confirm Transfer” button is a catastrophe. Modern strategies adopt risk-based prioritization. Teams must map their test cases to financial impact, ensuring that money-movement features—transfers, bill pays, and loan disbursements—receive the highest tier of mobile financial app automation and manual scrutiny. AI tools now assist this by identifying high-risk areas based on historical failure data, directing resources where business risk is highest.

2. Integrate Compliance Automation

Regulatory bodies do not care how fast you release; they care about audit trails. The days of manual security checklists are over. Banks must embed security testing for mobile financial apps directly into the CI/CD pipeline. This means automating checks for the OWASP MASVS (Mobile Application Security Verification Standard) every time a developer commits code. If a build fails a compliance check—such as leaving debug logs enabled—the pipeline should reject it automatically. This creates “audit-ready” evidence without manual compilation.

3. Scale Real Devices Strategically

Attempting to cover the entire Android ecosystem is a trap. While fragmentation is real, testing on 500 devices yields diminishing returns. The winning strategy is to maintain a focused matrix of 20–40 high-market-share devices. This “Golden Matrix” should cover the most popular devices for your specific user base, plus a selection of low-end legacy devices to catch resource leaks. This focused approach generally maintains crash-free rates above 99% without the overhead of testing thousands of hardware variations.

4. Embrace Agentic QA and Quantum Preparedness

Two emerging trends will define the next five years of fintech app testing:

- Agentic QA: We are moving beyond simple scripts to intelligent AI agents. These agents can perform autonomous compliance checks, automatically flagging UI changes that violate banking regulations or accessibility standards without human intervention.

- Quantum-Safe Security: Forward-thinking banks are already planning for the “Q-Day” threat—when quantum computers can break current encryption. Testing strategies must begin to include validation for quantum-safe cryptographic algorithms to future-proof data protection.

Ready to secure your banking app with our proven platform? Book your personalized Qyrus demo today and experience the future of fintech testing.

Frequently Asked Questions (FAQ)

Q: Why is real device testing critical for banking apps compared to emulators?

A: Only real devices provide full access to essential hardware sensors like Face ID, GPS, and NFC. These are required for secure login and contactless payments. Furthermore, emulators cannot accurately replicate the CPU throttling and battery drain that often cause crashes on older devices.

Q: What is the industry standard for mobile app security verification?

A: The OWASP MASVS (Mobile Application Security Verification Standard) provides the baseline security criteria for financial applications. It covers critical areas like data storage, cryptography, and authentication to ensure apps are resistant to attacks.

Q: How can automation help with biometric testing constraints?

A: Advanced tools like Qyrus allow for “Biometric Bypass” via instrumentation. This enables automated scripts to proceed past fingerprint or face checks without manual intervention, solving the bottleneck of automating secure login flows.

Q: What should be the priority when testing under “Economic Panic” conditions?

A: Testing should focus on Load and Stress Testing for unpredictable traffic spikes. Specifically, teams should measure RTO (Recovery Time Objectives)—how fast the system recovers after a crash—rather than just testing if it crashes.

Q: How do we handle third-party API failures during testing?

A: You must use API Mocking and Virtualization. Since you cannot control external systems (like credit bureaus), mocking allows you to simulate their responses—both success and failure—to ensure your app handles dependencies gracefully without crashing.