Varun RS

Varun RS

Application Programming Interfaces (APIs) are no longer just integration tools; they are the core products of a modern financial institution. With API calls representing over 80% of all internet traffic, the entire digital banking customer experience—from mobile apps to partner integrations—depends on them.

This market is exploding. The global API banking market will expand at a compound annual growth rate (CAGR) of 24.7% between 2025 and 2031. Here is the problem: the global API testing market projects a slower 19.69% CAGR.

This disparity reveals a dangerous quality gap. Banks are deploying new API-based services faster than their quality assurance capabilities can mature. This gap creates massive “quality debt”, exposing institutions to security vulnerabilities, performance bottlenecks, and costly compliance failures.

This challenge is accelerating toward 2026. A new strategic threat emerges: AI agents as major API consumers. Shockingly, only 7% of organizations design their APIs for this AI-first consumption. These agents will consume APIs with relentless, high-frequency, and complex query patterns that traditional, human-based testing models cannot anticipate. This new paradigm renders traditional load testing obsolete.

Effective banking API automation is no longer optional; it is the only viable path forward.

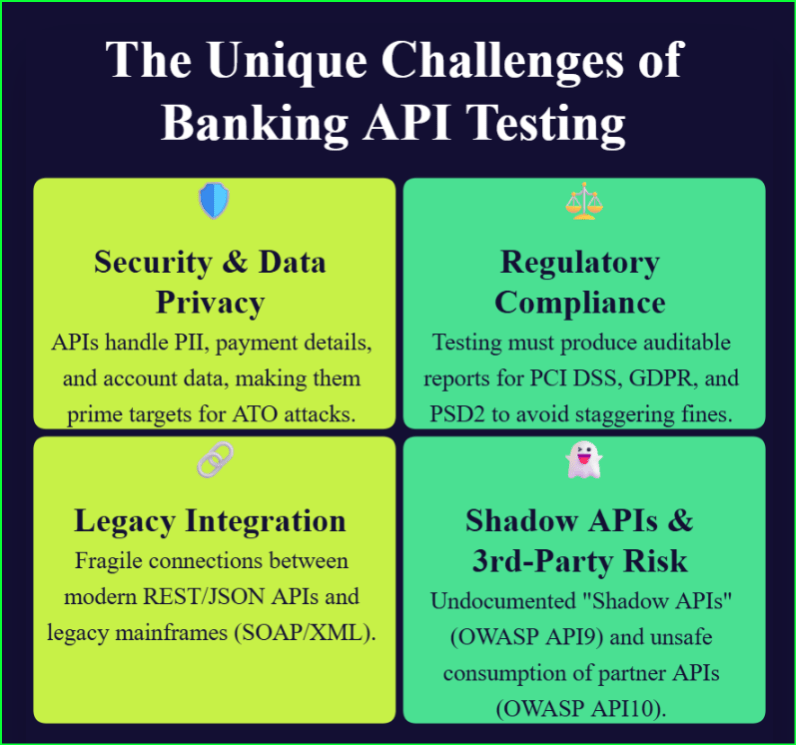

The Unique Challenges of Banking API Testing (Why It’s Not Like Other Industries)

Testing APIs in the banking, financial services, and insurance (BFSI) sector is a high-stakes discipline, fundamentally different from e-commerce or media. The challenges in API testing are not merely technical; they are strategic, regulatory, and existential. A single failure can erode trust, trigger massive fines, and halt business operations.

Challenge 1: Non-Negotiable Security & Data Privacy

API testing for banks is, first and foremost, security testing. APIs handle the most sensitive financial data imaginable: Personally Identifiable Information (PII), payment details, and detailed account data. Banks are “prime targets” for cybercriminals, and the slightest gap in authentication can be exploited for devastating Account Takeover (ATO) attacks.

Challenge 2: The Crushing Regulatory Compliance Burden

Banking QA teams face a unique burden: testing is not just about finding bugs but about proving compliance. Failure to comply means staggering financial penalties and legal consequences. Automated tests must produce detailed, auditable reports to satisfy a complex web of regulations, including:

- PCI DSS (Payment Card Industry Data Security Standard)

- GDPR (General Data Protection Regulation)

- PSD2 (Revised Payment Services Directive) in Europe

- US Regulations (like FFIEC, OCC, and CFPB)

A 2024 survey highlighted this, revealing that 82% of financial institutions worry about federal regulations, with 76% specifically concerned about PCI-DSS compliance.

Challenge 3: The Legacy-to-Modern Integration Problem

Financial institutions live in a complex hybrid world. They must connect modern, cloud-native microservices with monolithic legacy systems, such as core banking mainframes-built decades ago. The primary testing challenge lies at this fragile integration layer, where new REST API validation processes (using JSON) must communicate flawlessly with older SOAP API automation scripts (using XML).

Challenge 4: The “Shadow API” & Third-Party Risk

The pressure to bridge this legacy-to-modern divide is a direct cause of a massive, hidden risk: “Shadow APIs”. Developers, facing tight deadlines, often create undocumented and untested APIs to bypass bottlenecks. These uncatalogued and unsecured endpoints create a massive, unknown attack surface. This practice is a direct violation of OWASP API9:2023 (Improper Inventory Management).

Furthermore, banks rely on a vast web of third-party APIs for credit checks, payments, and fraud detection. This introduces another risk, defined by OWASP API10:2023 (Unsafe Consumption of APIs), where developers tend to trust data received from these “trusted” partners. An attacker who compromises a third-party API can send a malicious payload back to the bank, and if the bank’s API blindly processes it, the results can be catastrophic.

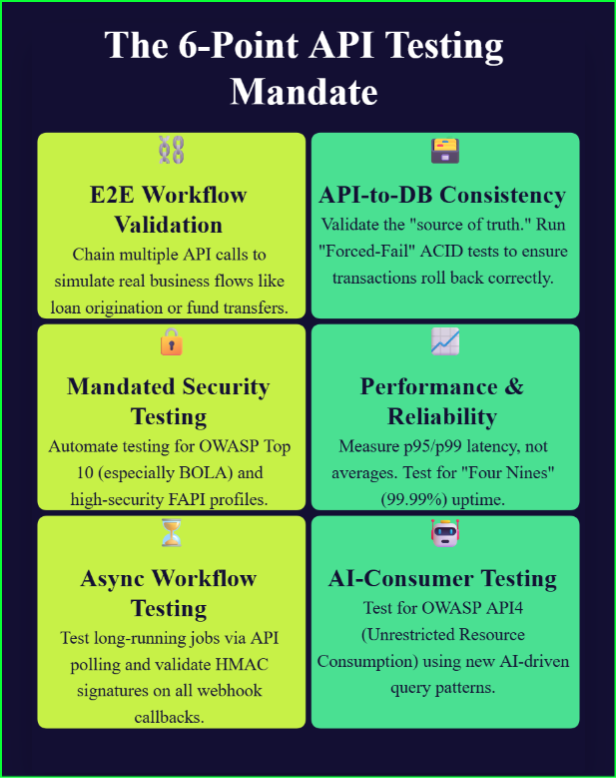

The 6-Point Mandate: An API Testing Strategy for 2026

To close the “quality gap” and secure the institution, QA teams must move beyond basic endpoint checks. A modern, automated strategy must validate entire business processes, from data integrity at the database level to the new threat of AI-driven consumption.

1. End-to-End Business Workflow Validation (API Chaining)

You cannot test a bank one endpoint at a time. The real risk lies in the complete, multi-step business workflow. API testing for banks must validate the entire money movement process by “chaining” multiple API calls to simulate a real business flow. This approach models complex, end-to-end scenarios like a full loan origination or a multi-leg fund transfer, passing state and data from one API response to the next request.

2. API-to-Database Consistency Checks (Testing ACID)

An API can return a “200 OK” and still be catastrop hically wrong. The ultimate test of a transaction is validating the “source of truth”: the core banking database. An API to database consistency check validates that an API call actually worked by querying the database to confirm the change.

The most critical test for this is the “Forced-Fail” Atomicity Test. Financial transactions must be “all-or-nothing” (Atomic).

- GIVEN: Account A has $100 and Account B has $0.

- WHEN: An API test initiates a $50 transfer.

- AND: Service virtualization is used to simulate a failure in a dependent service (e.g., the “credit Account B” service fails).

- ASSERT: The entire transaction must be rolled back. A database query must confirm Account A’s balance is still $100. If the balance is $50, you have failed the test and “lost” money.

3. Mandated Security Testing (OWASP & FAPI)

In banking, security testing is an automated, continuous process, not an afterthought. This means baking token-based authentication testing (JWT, OAuth2) and OWASP Top 10 validation directly into the test suite.

The “Big 4” vulnerabilities for banks are:

- API1: Broken Object Level Authorization (BOLA): The most common and severe risk.

- Test Case: Authenticate as User A (owns Account 123). Then, call GET /api/accounts/456 (owned by User B). The API must return a 403 Forbidden. If it returns 200 OK with User B’s data, you are critically vulnerable.

- API2: Broken Authentication: Test for weak password policies and JWT vulnerabilities.

- API5: Broken Function Level Authorization: Test if a standard user can call an admin-only endpoint (e.g., DELETE /api/accounts/456) .

- API9: Improper Inventory Management: The “Shadow API” problem we covered earlier.

For Open Banking, standard OAuth 2.0 is not enough. Tests must validate the advanced Financial-grade API (FAPI) profile and DPoP (Demonstrating Proof of Possession) to prevent token theft.

4. Performance & Reliability Testing (Meeting the “Nines”)

Averages are misleading. The only performance metric that matters is the experience of your worst-perceiving users. You must measure p95/p99 latency—what the slowest 5% of your users experience.

Understand the “Cost of Nines”:

- 99.9% (“Three Nines”): Allows for ~8.7 hours of downtime per year. For a bank, this is a catastrophic business failure.

- 99.99% (“Four Nines”): Allows for ~52 minutes of downtime per year. This is the new minimum standard.

Your endpoint latency monitoring must use realistic, scenario-based load testing, not generic high-volume tests. Simulate an “end-of-month processing” spike or a “market volatility event” to find the real-world bottlenecks.

5. Asynchronous Workflow Testing (Polling, Webhooks & Queues)

Many banking processes (loan approvals, transfers) are not instant. You must test these asynchronous flows.

- Asynchronous API Polling: For long-running jobs, the test script must call a status endpoint in a loop (e.g., GET /api/loan_status/123) until a “COMPLETED” status is received, measuring the total time elapsed.

- Webhooks: To validate notifications from third parties (e.g., payment gateways), the most critical test is security. A webhook URL is public, so you must validate the HMAC signature. Your test must assert that any request with a missing or invalid signature is rejected with a 401/403 error.

- Message Queues: Test internal data streams (like Kafka) for guaranteed delivery and data integrity at scale.

6. The New Frontier: Testing for AI Consumers

This is the new strategic threat for 2026. As noted, only 7% of organizations design APIs for AI-first consumption. AI agents will consume API-driven BFSI systems with relentless, high-frequency query patterns that will break traditional models.

This demands a new “AI-Consumer Testing” paradigm focused on OWASP API4:2023 (Unrestricted Resource Consumption).

- Bad Test: “Can I get a loan quote?”

- Good Test (AI-Consumer): “Can I request 10,000 different loan quotes in one second?”

This test validates your rate-limiting and resource-protection controls against the specific patterns of AI agents, not just malicious bots.

The “Two Fronts” of API Governance: Managing Legacy & Modern Systems

To manage the complexity of a hybrid environment, banks must fight a war on two fronts. A mature API-driven BFSI system requires two distinct governance models—one for external partners and one for internal microservices.

The External Front (Top-Down): OpenAPI/Swagger

For your public-facing Open Banking APIs and third-party partner integrations, the bank must set the rules as the provider.

The OpenAPI (Swagger) specification serves as the non-negotiable, provider-driven “contract”. This specification is the single source of truth that allows you to enforce consistent design standards and automate documentation. This “contract-first” approach is the foundation for API contract testing (OpenAPI/Swagger), where you can automatically validate that the final implementation never deviates from the agreed-upon specification.

The Internal Front (Bottom-Up): Consumer-Driven Contract Testing (Pact)

For your internal microservices, a top-down model is too slow and rigid. Traditional E2E tests become brittle and break with every small change.

This is where Consumer-Driven Contract Testing (CDCT), using tools like Pact, is superior. This model flips the script: the “consumer” (e.g., the mobile app) defines the exact request and response it needs, which generates a “pact file”. The “provider” (e.g., the accounts microservice) then runs a verification test to ensure it meets that contract.

This is a pure automation game. It catches integration-breaking bugs on the developer’s machine before deployment, enabling CI/CD pipelines to run checks in minutes and eliminating the bottleneck of slow, complex E2E test environments.

A mature bank needs both: top-down OpenAPI governance for external control and bottom-up CDCT for internal speed and resilience.

Solving the Un-testable: The Critical Role of Service Virtualization

The most critical, high-risk scenarios in banking are often impossible to test. How do you safely run the “Forced-Fail” ACID test from Section 3? How do you performance-test a third-party API without paying millions in fees? And how do you run a full regression suite when the core mainframe is only available for a 2-hour nightly window?

The answer is Service Virtualization (SV).

SV (or “mocking”) solves the test-dependency problem. It allows you to simulate the behavior of these unavailable, costly, or unstable systems. Instead of testing against the real partner API, you test against a “virtual” version that is available 24/7, completely under your control, and can be configured to fail on demand.

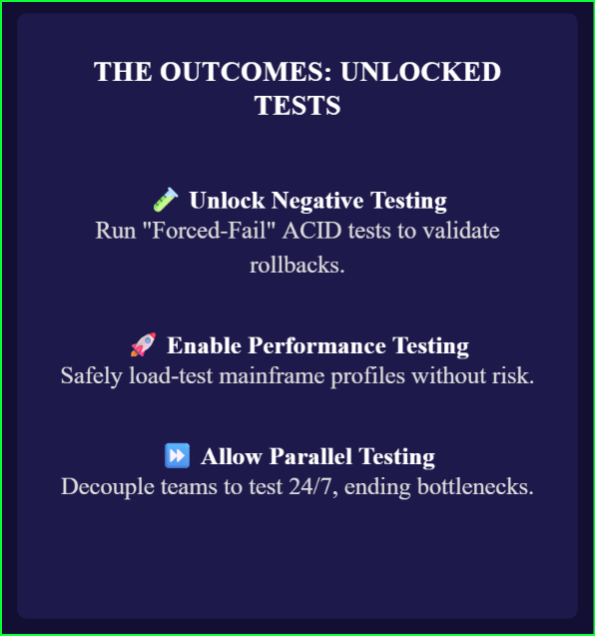

This capability unlocks the testing strategies that banks must perform:

- Negative Testing: SV is the only way to reliably run the “Forced-Fail” ACID Atomicity test. You can configure the virtual service to return the 500 error needed to validate your system’s rollback logic.

- Performance Testing: You can finally load-test the “un-testable.” SV allows you to simulate the performance profile of the mainframe, capturing bottlenecks without any risk to the real system.

- Parallel Testing: It decouples your teams. The mobile app team can test against a virtual core banking API without waiting for the mainframe team, enabling true parallel development.

The business case for SV is not theoretical; it is proven by major financial institutions.

- Speed: A report covering over 20 financial institutions, including Bank of America, found that projects using SV deliver software 40% faster.

- Efficiency: An ING case study showed that by virtualizing key dependencies, their test environment setup and execution time was reduced from 5 days to 1 day.

- Cost: Accenture reports that SV reduces infrastructure costs by 20-40% by minimizing reliance on expensive, shared-test environments.

Accelerate Your API Banking Automation with Qyrus

The challenges are significant, but the “quality gap” is solvable. Closing it requires a platform that is built to handle the specific, hybrid, and high-stakes nature of API-driven BFSI systems. Manual testing and fragmented, code-heavy tools cannot keep pace. A unified, AI-powered platform is the only way to accelerate banking API automation and ensure quality.

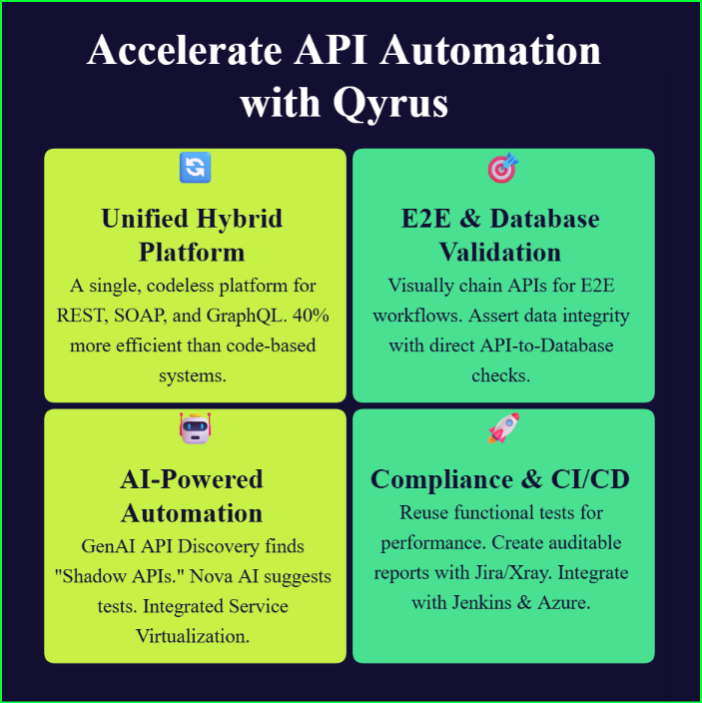

A Unified Platform for a Hybrid World

The core legacy-to-modern integration problem (Challenge 3) requires a single platform that speaks both languages. Qyrus is a unified, codeless platform that natively supports REST, SOAP, and GraphQL APIs. This eliminates the need for fragmented tools and empowers all team members—not just developers—to build tests, making testing with Qyrus 40% more efficient than code-based systems.

Solve End-to-End & Database Testing Instantly

Qyrus directly solves the most complex banking test scenarios, Strategies 1 and 2.

- API Process Testing: This feature directly maps to E2E Business Workflow Validation. A visual, drag-and-drop canvas allows you to chain APIs together to test complex money movement flows, passing data from one call to the next.

- API-to-Database Assertion: This feature is built to solve the API-to-Database Consistency problem. You can visually map an API request or response directly to a database (like Oracle, PostgreSQL, or DB2) and assert that the transactional data is correct.

AI-Powered Automation to Close the Quality Gap

To overcome the “Shadow API” problem (Challenge 4) and the new AI-Consumer threat (Strategy 6), you need AI in your testing arsenal.

- Service Virtualization & API Builder: Qyrus provides robust Service Virtualization to run the “Forced-Fail” ACID tests and mock 3rd-party dependencies. Its GenAI-powered API Builder can even create a new virtualized API from just a text description, letting your teams test before the real service is even built.

- API Discovery: Qyrus’s AI-powered browser extension directly solves the “Shadow API” (OWASP API9) problem. It records network traffic as you browse your application, discovers all APIs (even undocumented ones), and automatically generates test scripts for them.

- Nova AI: Qyrus’s AI assistant accelerates test creation by autonomously analyzing an API response and suggesting assertions for headers, schemas, and body content, ensuring comprehensive coverage.

Built for Performance, Compliance, and CI/CD

Qyrus completes the strategy by integrating endpoint latency monitoring and compliance reporting directly into your workflow.

- Integrated Performance Testing: You can reuse your functional API tests as Performance Tests. This allows you to run realistic, scenario-based load tests and validate your p99 latency targets, capturing key metrics like hits per second and response times over time.

- Jira & Xray Integration: Qyrus integrates directly with Jira and Xray. When tests run, the results are automatically pushed back, creating the crucial, auditable report trail required for regulatory compliance (Challenge 2).

- CI/CD Integration: Native plugins for Jenkins, Azure DevOps, and other tools enable true banking API automation within your pipeline, shifting quality left.

Conclusion: From “Quality Gap” to “Quality Unlocked”

The stakes in financial services have never been higher. The “quality gap”—caused by rapid API deployment, legacy system drags, and new AI-driven threats—is real.

Manual testing and fragmented, code-heavy tools are no longer a viable option. They are a direct risk to your business.

The future of API testing for banks requires a unified, codeless, and AI-powered platform. Adopting this level of automation is not just an IT decision; it is a strategic business imperative for security, compliance, and survival.

Ready to close your “quality gap”? See how Qyrus’s unified platform can automate your end-to-end API testing—from REST to SOAP and from security to performance.

March 24, 2026

March 24, 2026  10 min

10 min

![Featured_Image-LLM_evaluation[1]](https://www.qyrus.com/wp-content/uploads/2026/03/Featured_Image-LLM_evaluation1.webp)